Zespri is launching a discussion with growers on how we respond to a more challenging and competitive China market, where consumers are increasingly demanding when it comes to fruit quality.

China is our largest and highest-value market, and we have strong confidence in its future. However, like much of China, the premium fruit category is changing quickly.

There are four key trends in the market:

Increasing competition: Supply of fruits like durian, cherries and blueberries (domestic and imported) has increased significantly, with prices for some of these products dropping by up to 40% because of oversupply. With Zespri holding our premium pricing, the gap between us and competitors has widened.

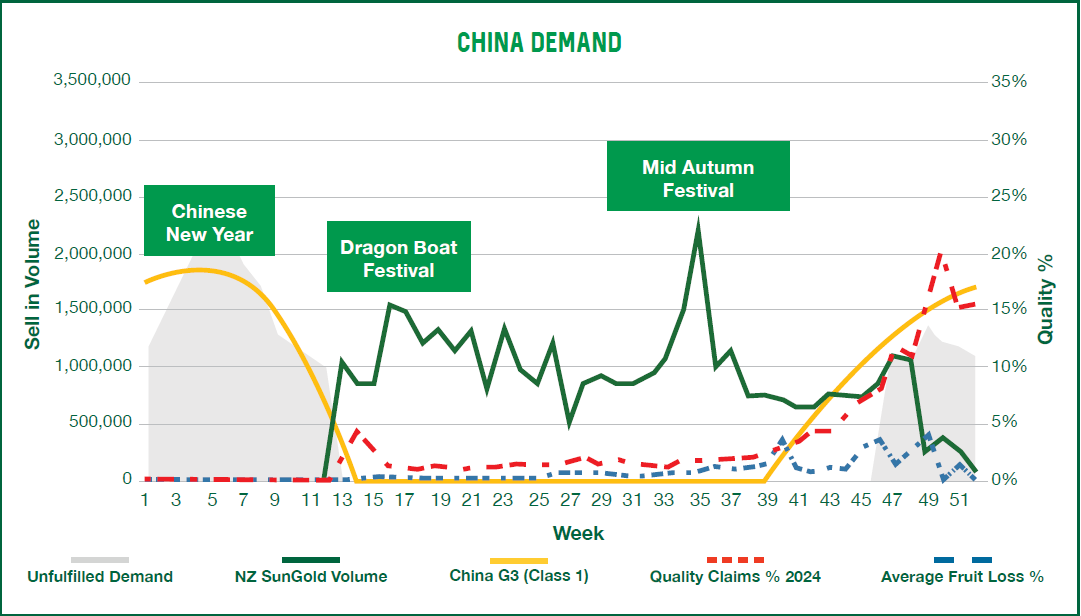

Variability in our quality: Particularly late in the season, quality variability is impacting customer confidence. In 2025, claims on fruit sold from November reached as high as 22% – more than one in five pieces of fruit failed to meet our standards. Customers have been clear that this level of inconsistency is not acceptable, particularly when consumers have more choice and are comparing Zespri against other premium fruits and fresher local G3.

More selective consumers: Consumers are generally becoming more selective at the end of the New Zealand season. A softer economic environment is seeing shoppers place greater emphasis on value. Eating quality and price are under closer scrutiny as consumers compare options and make more discerning choices. Our customers and consumers are far less accepting of any fruit that is not of the highest quality, particularly in the latter part of the selling season.

Continuing improvement of local G3 supply: Chinese-grown G3 is now available from September through to March, with improving quality, brands and sales. In key markets like Shanghai, consumers effectively have a 12-month supply of G3 between New Zealand and Chinese fruit, meaning they have more choice. Without exclusive access to supply throughout the year, we have less ability to control our sales channels.

While Zespri is maintaining our pricing and position, these trends threaten our ability to remain the leader in the category, maintain premium value and deliver sustainable long-term returns.

Our premium depends on trust. If customers and consumers cannot rely on Zespri to consistently deliver the eating experience they expect, they have a clear reason to switch. We are receiving feedback that confidence in Zespri’s ability to consistently deliver premium quality throughout the entire selling window is being tested.

To respond, Zespri is considering how best to keep high-quality Zespri Kiwifruit in front of consumers year-round, while always prioritising New Zealand fruit and protecting grower returns. We have identified two broad options and are seeking grower feedback on our next steps, whether that is through these pathways or alternatives.

One option is to continue competing from New Zealand, with our response built around improving late-season quality, investing in post-harvest innovation, and developing longer-storing varieties over time.

A second option is a tightly controlled China Supply procurement model to complement New Zealand fruit. Under this approach, New Zealand fruit would be sold for as long as it meets the quality and customer expectations required to protect the Zespri premium. If late-season quality falls below that level, Zespri would have the option to transition to locally grown G3 that meets Zespri’s quality, maturity and food-safety requirements, with additional oversight in-market.

The procurement option is similar to our existing model for ZGS Green, where we procure Hayward from both Italy and Greece. The decision on when to transition would be based on quality and customer-confidence indicators — including firmness, defects, claims and customer feedback — with the objective of maximising New Zealand grower returns while protecting the Zespri brand. The principle is that we should only put fruit in front of consumers when it supports the Zespri brand and the premium growers depend on.

Under this approach, all fruit would be required to meet Zespri’s quality, maturity and food-safety requirements, with additional oversight in-market. Any China Supply model would require grower support through a Producer Vote, which, depending on feedback, could be something we consider in 2027.

Over the next few months, we will be sharing information with growers on the changing China market and our options, answering questions and seeking feedback on your preferred way forward.

There are risks associated with both options that we need to consider, including concerns around brand integrity, intellectual property, and the consequences of not responding strongly enough. These would be carefully worked through as part of our discussions.

This is one of the topics at our upcoming Shed Talks, so please join us so that we can understand your views. Your feedback will play a key role in shaping the next steps.

Click top right to enlarge image

Click top right to enlarge image

China market facts

- NZD $1.4b in sales in Greater China in 2025/26

- 300,000 stores across China

- Zespri is the number one fruit brand

- Durian volumes up from 100,000 tonnes in 2025/26 to 260,000 tonnes this year, with prices down up to 40%

- Estimated between 7100 and 8100 hectares of G3 in the ground in China, with Class 1 packout rate of 70 - 80% and improving quickly

Was this page helpful?